Is your manufactured foundation acceptable to lenders?

Published on May 05, 2025 | Manufactured home loans

Is your manufactured foundation acceptable to lenders?

Why the California HCD433 isn't evidence the foundation is ok for lenders.

Many agents and buyers/sellers erroneously assume if a HCD433 (California form) has been recorded against the property it is evidence of a manufactured home having been properly installed on a foundation that's acceptable for all loan programs. This common misconception can cause lots of frustration and possibly end with a cancelled transaction.

What's a HCD433?

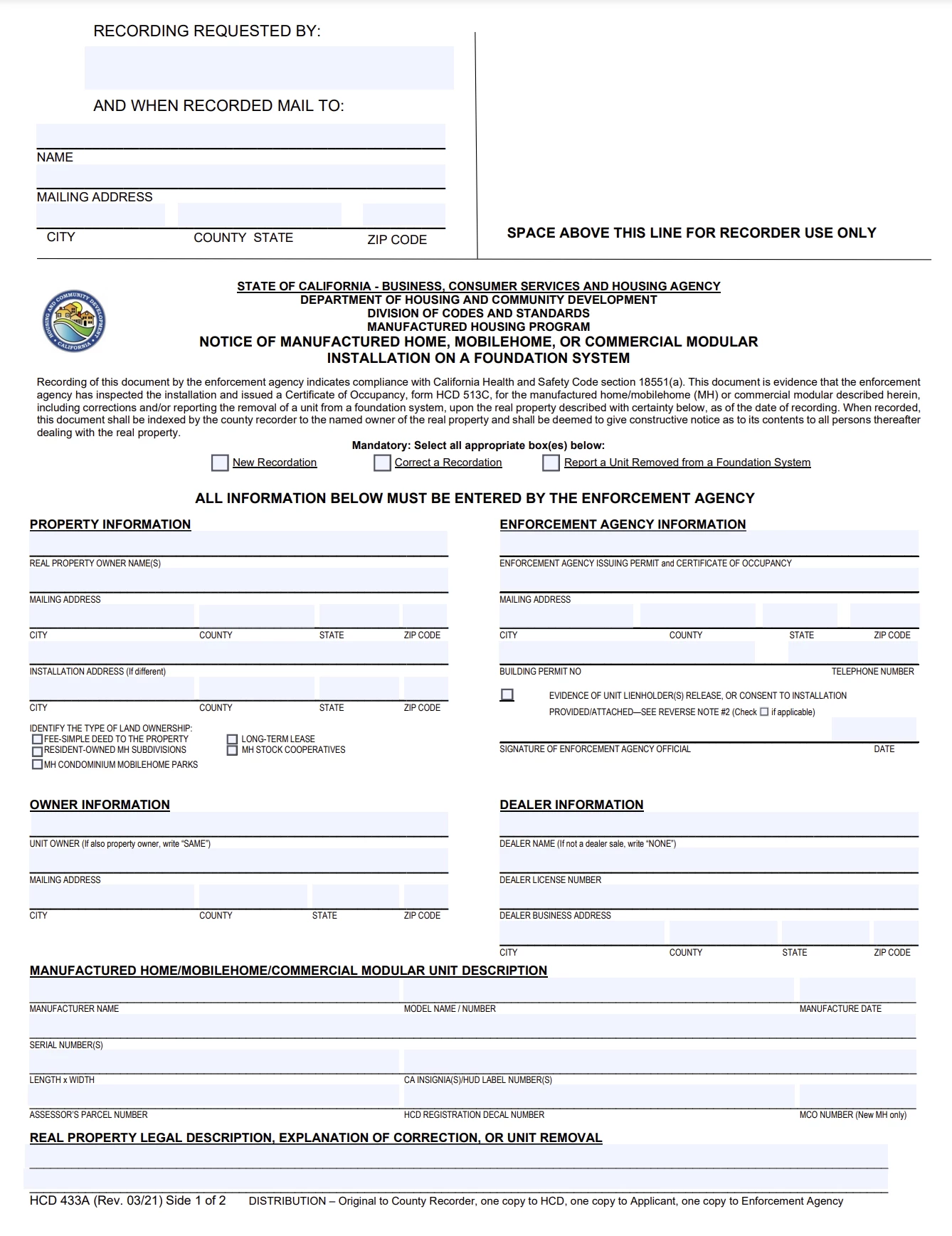

The HCD433 is a set of California forms with 2 very different versions we'll discuss here. When a 433 is recorded it accomplishes one and possibly 2 things. The first is to convert the manufactured home from personal property to "a fixture improvement to real property" thus the improvements and land would be taxed as real property by the respective county. If the correct lender required HCD433A is used, this indicates the home was installed on a foundation system---but does not --by its self --prove it's a foundation type acceptable to lenders.

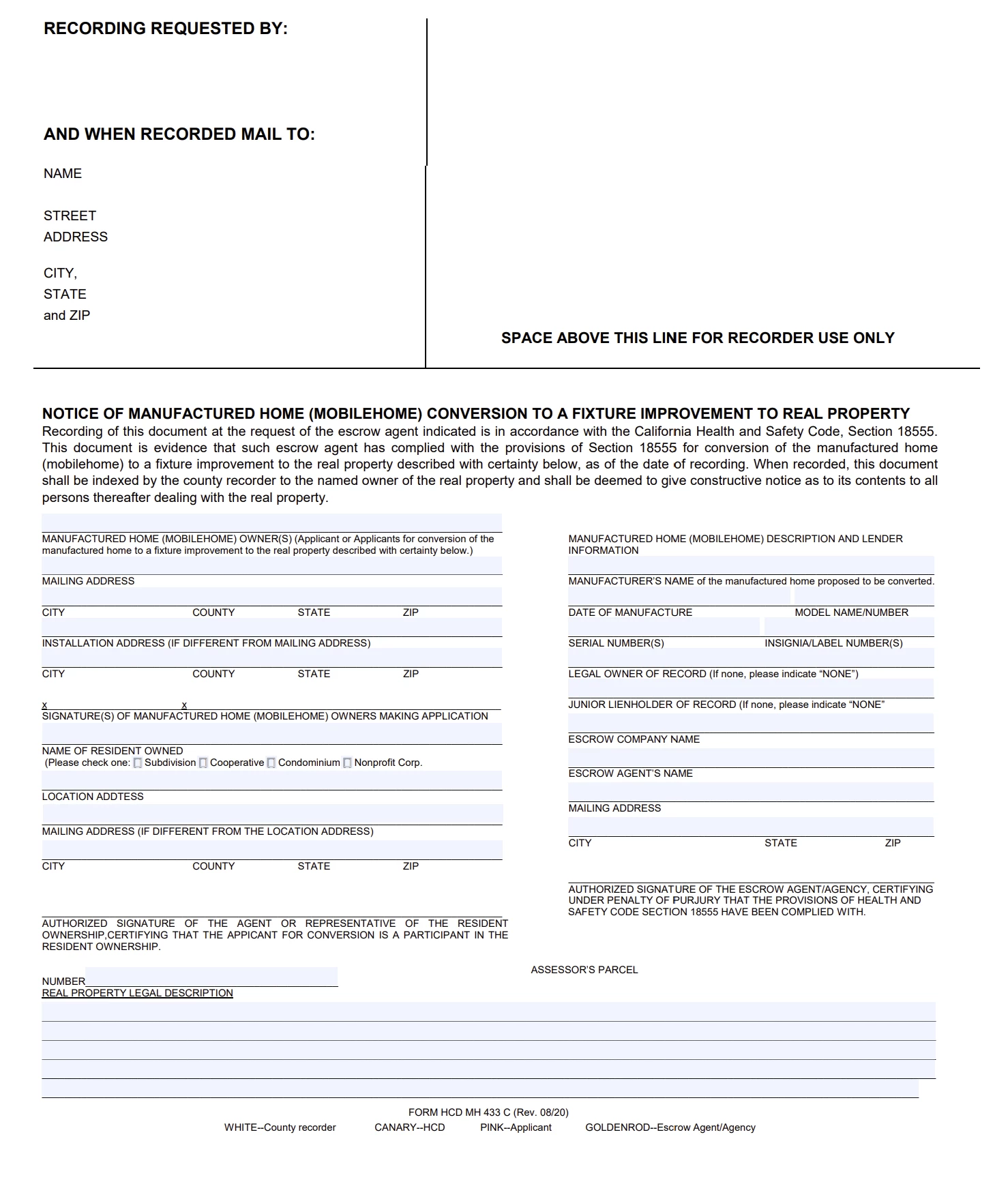

A different type of HCD433 -- the HCD433C -- only confirms the transfer of the manufactured home to the real property tax rolls-and does not certify it was installed on a "permanent" foundation system. Property owners, agents and even county recorder peeps can occasionally get these 2 types of HCD433s confused.

Here is a copy of a HCD433A.

Here is a copy of a HCD433C

So if the 433 isn't absolute proof, how do you know a manufactured home's foundation system is acceptable to lenders? Great question --read on for some additional info.

Potential problems related to the acceptability of a foundation system for a particular loan program can arise based on the type, current condition and construction quality of the foundation used for the manufactured home.

In my 30+ years financing hundreds of manufactured homes -both new construction and resale-- I have seen a variety of different foundation systems, some acceptable to lenders at the time of installation--that are not now--and others that experienced a substandard foundation installation and are now in need of repair/modification to be acceptable to a lender.

Conventional loan foundation requirements

On conventional loans, an appraiser typically must include in the appraisal report their opinion the home was installed in accordance with the manufacturer's requirements for anchoring, support, stability and maintenance and the foundation system is compliant with Fannie Mae and/or Freddie Mac standards. If the appraiser notices issues with the foundation and is unwilling to confirm it is compliant, a licensed structural engineers' inspection and their foundation certification letter would be required.

VA loan foundation requirements

VA requires the appraiser to state the home is permanently affixed to a foundation system conforming to the VA's Permanent Foundations guide for Manufactured Housing Standards. Again, if the appraiser is unwilling to confirm this, an engineer's inspection and foundation certification letter would be required.

FHA and USDA foundation requirements

On FHA and USDA loans a licensed engineers' foundation certification letter is mandatory. Occasionally this engineer's letter can be a previous one, however it depends on how old the letter of certification is, along with any improvements/changes made to the home after the date of the certification letter. For example, a 10 year old manufactured home was financed with an FHA loan and the current owner has a copy of an engineer's cert letter completed at that time. However, the home had some type of addition or modification in the past few years. This scenario would require a new engineer's certification letter be provided to be eligible for a new FHA purchase loan.

Foundation skirting All loan types must comply with HUD codes. Non-bearing skirting must be permanently attached to concrete, masonry, or treated wood backing. The skirting must allow for ventilation of space. Specifics can be found in the HUD Mortgagee Letter 2009-16. Link to that letter here.

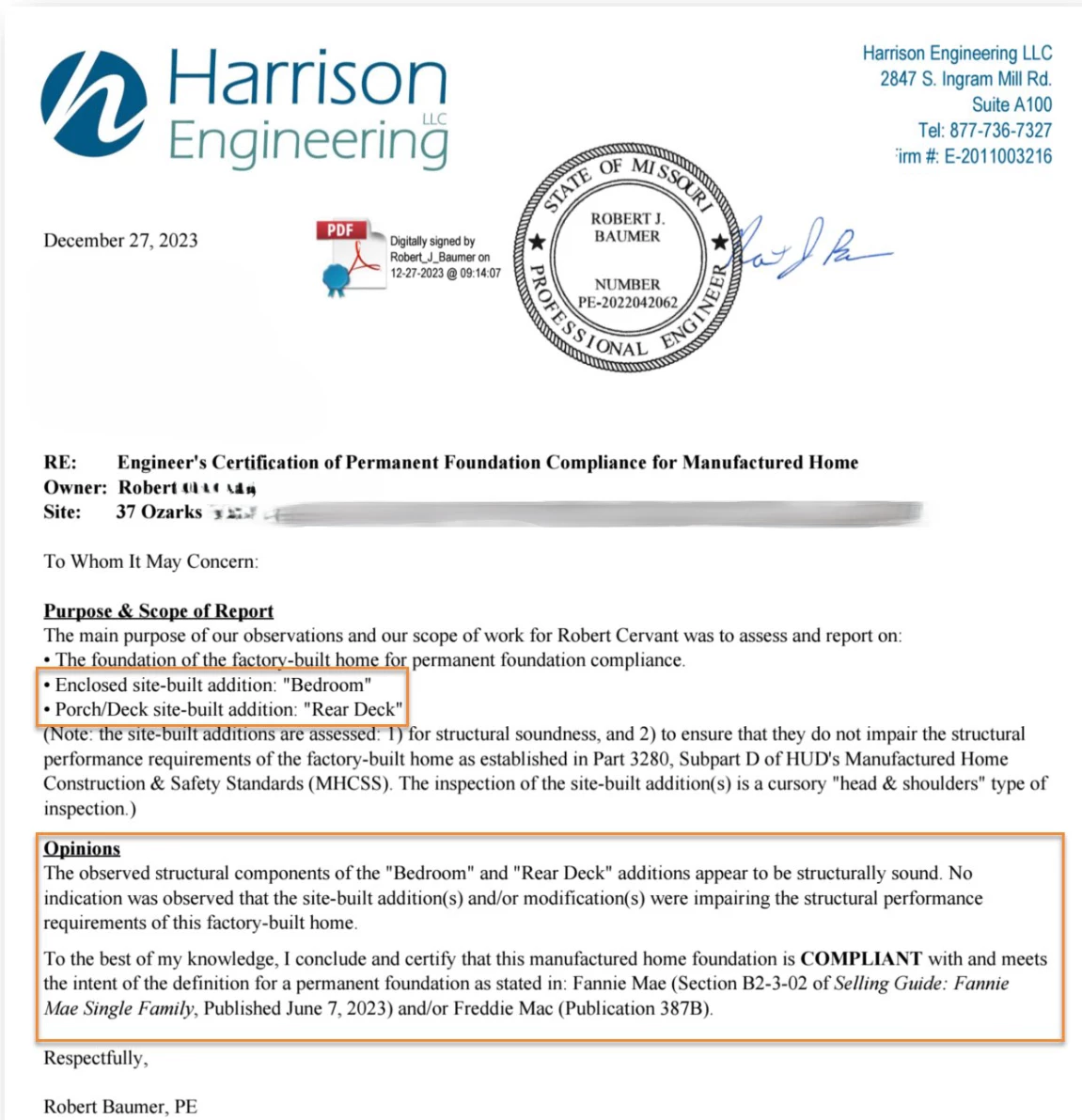

How to get an engineer's Foundation certification

An engineers' foundation certification letter --sample below-- can be ordered from any licensed structural engineer, however most experienced with manufactured loan officers will have a source to order from.

Cost varies based on location and complexity of the foundation/home, but a typical fee is about $600 to as much as a $1000 or more in our area. Timeframe from order/payment date to receipt is about one to two weeks depending on property location and complexity. If upon inspection, the engineer can't issue a certification they typically will provide a report of what needs to be done to make the foundation compliant.

In my experience, any foundation repair or retrofit to meet loan program and lender's standards can typically cost hundreds to thousands of dollars depending on the scope of the work needed and take several weeks to complete. Once the work is completed a reinspection is typically required with an additional inspection fee.